Mortgage Brokers vs Lenders

In this guide, we will cover the difference between Mortgage Brokers vs Lenders when buying or refinancing a home, investment property, or commercial real estate. There can be advantages of using mortgage brokers vs lenders and vice versa. I highly recommend consumers due their due diligence when interviewing mortgage companies and loan officers. All mortgage loan applicants need to be provided with a Loan Estimate (LE) three business days from the date the loan application was submitted.

More than likely, your interest rate will not be locked so the loan officer will come to a guestimate rate. Remember that there is no such thing as free in the mortgage industry.

The higher the compensation of the mortgage company, guess who will be paying for the higher yield-spread premium? You the consumer are. Who has higher rates between Mortgage Brokers vs Lenders? In general, lenders have higher compensation than the maximum of 2.75% mortgage brokers are capped by law. Some of the first decisions you’ll make when getting ready to buy a home involve determining who will help you secure financing. Two professionals are dominant in this arena: mortgage brokers and mortgage bankers. While both can assist you in getting a home loan, they function quite differently from one another, offering different advantages depending upon your situation.

Ready to compare real offers—without the guesswork?

Get a free, side-by-side mortgage review and see the real difference in rates, fees, and total closing costs between a mortgage broker and a direct lender.

What is a Mortgage Broker?

A mortgage broker is an intermediary between a borrower and a lender. They do not lend directly from their funds. They have relations with several lending institutions and work to find the exact loan product that best fits your financial profile.

Brokers earn their income through commissions paid by either the lender, the borrower or sometimes both. A loan broker enables borrowers to hook up with creditors.

Mortgage brokers are certified to transact with specific creditors and refer a home loan or any other real estate loan that suits the purchaser’s financial ability well. Mortgage brokers help reduce the purchaser’s fee by researching and finding unique listings in the market place. The mortgage broker also acts as the intermediary in preparing the paperwork and documentation for the loan

What is a Mortgage Banker?

A mortgage bank is an individual or organization that originates home loans. Many home mortgage traders produce profits by charging borrowers an origination fee. A loan banker is a real estate agent who serves as the originator of the loan. They mortgage their budget to authorized borrowers.

Mortgage bankers offer borrowers options with varying interest rates to choose from. The mortgage quantity that a loan bank can approve will highly depend on the borrower’s credit score records and financial capability.

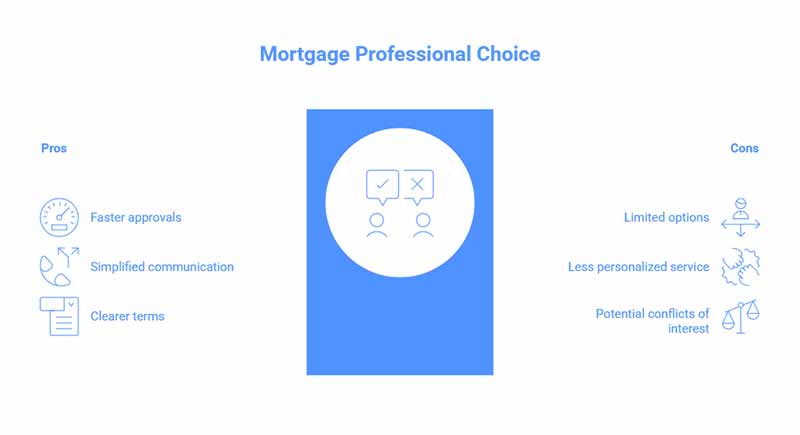

Mortgage bankers offer a range of mortgage options with varying interest rates to generate income. They provide the mortgage using their own funds and may retain the loan or sell it on the secondary market. Because mortgage bankers maintain control of the loan process internally, they may often grant faster approval and closing times. However, their loan offerings are dictated by the products their institution offers, which can limit options given to borrowers compared to those available through brokers.

How to Decide Between Mortgage Brokers vs lenders

Picking a mortgage professional depends on evaluating your priorities, financial situation, and preferences for loan options and service style.

Start with your situation

- If you’re in a hurry to get an approval and your loan processing smoothed out, mortgage lenders could give you faster approvals because they process everything in-house.

- Otherwise, if you are self-employed with little to no adjusted gross income due to large unreimbursed expenses, changing income, had a recent credit setback, have a large student loan balance, and high debt-to-income ratio, a mortgage broker would be the best professional for the job.

- Self-employed borrowers purchasing an upscale luxury home and need a jumbo loan, a mortgage broker would be the best professional where the MLO can shop dozens of wholesale lenders specializing in non-QM loans that use alternative source of income rather than traditional income tax returns.

- Ideal non-QM jumbo loans include bank statement loans, Asset-Depletion mortgage loans, P and L statement loans, No-Doc loans, and sometimes there are non-QM wholesale lenders that only use one year tax returns for self-employed borrowers who have been in business for five years or long.

Consider Your Comfort with Personalized Service

- With a mortgage broker, you will often get more personalized attention to walk you through various lenders and comparisons of terms.

- Mortgage bankers are direct lenders and, while there may be less variation, they can simplify communications by handling all steps in-house.

Assess fee structures and transparency

- Brokers are often paid by the lender at close, which makes their service free to you but may very well be a factor in the loan products they recommend.

- Mortgage bankers charge fees directly or bundle costs into the loan terms; understanding all associated expenses up front is crucial to avoid surprises.

Understand potential conflicts of interest

- While brokers provide choice, their compensation model could bias recommendations toward lenders that pay higher commissions.

- The limited product range of mortgage bankers may not always secure the best market rates, but being aligned with one institution can result in clearer terms and conditions.

When to Choose a Mortgage Broker

Consider working with a broker if you:

- Have an individual financial situation that may not fit into typical lending criteria.

- Want to compare offers of multiple institutions without applying separately to each.

- Value having an advocate to explain the complex differences in the loan products.

- Are you a first-time homebuyer who could benefit from education about various options?

- Have less-than-perfect credit and need someone to find lenders specializing in your situation.

When to Choose a Mortgage lender

A mortgage Lender may be your best option if you:

- Have an existing relationship with a bank that gives mortgage services.

- Easily qualify for traditional loans and prefer simple processing.

- Value the convenience of having all of your financial services in one place.

- Want direct access to the institution that will make the lending decision.

- Are comfortable with less selection in return for simplicity

Neither mortgage broker nor mortgage banker is inherently better. It simply depends on your individual financial scenario, the level of guidance you need, or the level of service that appeals to you. Some borrowers appreciate the thorough shopping approach that brokers provide, while others understand and like the direct relationship and institutional clout that comes with mortgage bankers.

A lot of successful homebuyers actually consult with both types of professionals before making a decision, using initial consultations to gauge who offers the best combination of rates, service, and trustworthiness for their specific needs.

Keep in mind that this is probably the largest financial transaction of your life-investing some time to understand your financing options will pay dividends not only in the short but also the long run.

Mortgage Brokers vs lenders

Now, to wrap up the discussion about the difference between mortgage brokers vs lenders, please refer to the following points.

- Real estate agents and other professionals refer borrowers to mortgage brokers and lenders when their clients need a home loan.

- Both mortgage brokers and lenders need to be licensed and offer services to individual or business clients.

- Mortgage brokers is an intermediary between wholesale mortgage lenders and borrowers in the real estate market, while mortgage lenders originates, underwrites, and funds mortgage loans with their warehouse line of credit.

- Mortgage brokers help clients find top-notch deals in the market.

- Mortgage brokers can have dozens of wholesale lenders in their lending partner network.

- Wholesale mortgage lenders are normally not licensed and cannot originate loans directly to consumers.

- Wholesale mortgage lenders need to form a partnership agreement with a NMLS licensed mortgage company.

- Mortgage bankers offer unique mortgage options, each with its amount of interest.

- Loan origination, according to the Corporate Finance Institute, entails the risking of capital by mortgage lenders to fund loans.

- Additionally, mortgage lenders do not have to disclose their compensation (Yield-Spread Premium) unlike mortgage brokers need to disclose the yield-spread premium on the closing disclosure.

- Mortgage brokers are capped at 2.75% YSP for the mortgage brokerage company and the loan officer gets a percentage of the 2.75%,

- Mortgage lenders cannot survive with a 2.75% yield spread premium due to overhead.

- The amount of commission lenders charge depends on the lender and since lenders are exempt from disclosing their compensation, it is difficult to mark a uniform value like it is done for mortgage brokers.

- Consumers need to realize that the higher the compensation the lender makes, the higher the mortgage rate to the borrower.

- Even loan officers who work at lenders do not know how much their employer makes on a loan transaction.

- If you want transparency with the best rates and hundreds of mortgage loan options, hiring mortgage brokers vs lenders is what we would recommend.

- In contrast, mortgage brokers originate loans in the name of financial institutions and organizations.

- Under federal and state laws related to full disclosure, mortgage brokers are required to show the additional cost(s) charged to the buyer.

FAQ On Mortgage Brokers Vs lenders

Can mortgage lenders work in any type of financial institution?

- Yes. Mortgage lenders may work for a large national bank, a regional bank, a credit union, an online lender, or even a mortgage company specializing in mortgages only.

- Loan officers hired by an FDIC bank, or credit union do not need to get licensed.

- Loan officers working for an FDIC bank or credit union just need to get registered with the NMLS and are exempt from taking the 20 hour CE NMLS Course, and are exempt from taking the 125 question federal NMLS examination.

- Whichever the case, loan officers working for lenders are captive registered MLOs and are often limited to selling the lender;s sole product or products and may have a limited number of wholesale mortgage lending partners.

Are mortgage brokers licensed?

- Yes.

- Mortgage brokers must obtain state licenses in each state where they conduct business.

Who pays the mortgage broker?

Compensation for brokers may come in several ways:

-

- The lender may pay them; you may directly pay compensation to them, known as borrower-paid compensation; or a combination of both may occur.

- In any case, by law, brokers are mandated to disclose their compensation method.

Mortgage Brokers vs Lenders: Who Charges More On a home loan

- Not necessarily. While brokers may charge origination fees, they often find loans with lower rates or better terms that offset their fees.

- Mortgage lenders also incur costs through various fees and rate pricing in their loans.

- The total cost depends upon the particular loan offer, not the type of professional.

what type of mortgage company is easier to negotiate fees and rates between Mortgage Brokers vs lenders

- Yes, many fees are negotiable with both brokers and lenders.

- Make the request for fees to be reduced or eliminated, based on competing offers or significant business being introduced into the institution.

Do I need to fill out several applications if I use a mortgage broker?

- No, that’s one of the advantages of using a mortgage broker-you fill out one application and they send it to a number of lenders on your behalf.

- This not only saves time but also means uniformity across submissions.

Can I Work With Both A Broker And Banker Simultaneously?

- You can explore options with both, especially in the pre-approval and shopping phase.

- Then, when you move forward, you’d want to go with one to avoid confusion and so you don’t have numerous credit inquiries that may ding your score.

- A mortgage broker can shop the best rate and terms for you loan with multiple if not dozens of wholesale lenders.

Whom should I call if I have questions after closing?

- Your loan is usually serviced either by the same lender who originated the loan, or the loan is sold to a company servicing the loan.

- Your broker will not be involved in ongoing servicing.

- However, your lender’s institution may retain servicing, and you may have a continued relationship.

I’m self-employed with complicated taxes – who should I use?

- This is where mortgage brokers usually tend to shine, as they know which wholesale mortgage lenders specialize on non-QM and alternative mortgage loan options who specialize in self-employed borrowers and have more flexible documentation requirements.

- They can match your unique profile to suitable lenders, rather than applying to institutions where you’re likely to be declined.

Can I change mid-process from broker to banker or vice versa?

-

- Yes, though it will delay your closing as you will in essence be starting over with a new application.

- Switch only if there is a compelling reason such as significantly better terms elsewhere, or serious service problems with your current professional.

Not sure if you should use a broker or a lender for your situation?

Whether you’re self-employed, buying an investment property, refinancing, or rebuilding credit, we’ll match you with the best option and explain your choice.