Bank Statement Loans: What They Are and How They Work

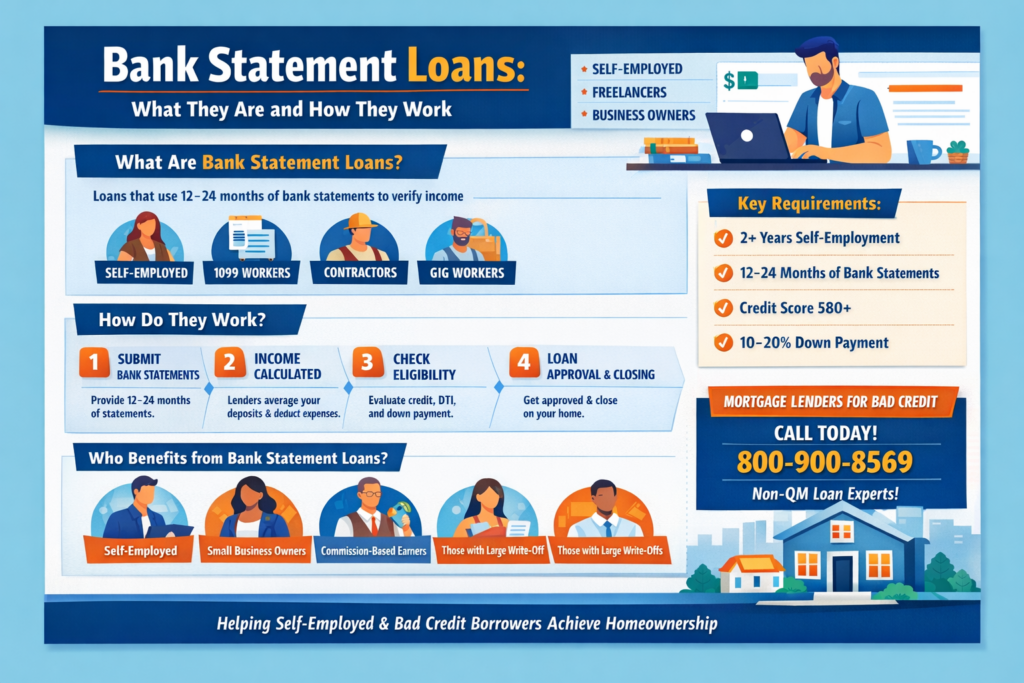

Bank statement loans help freelancers, gig workers, contractors, and business owners who want a mortgage but do not have W-2s or paychecks. Instead of the usual proof, your bank deposits serve as proof of your income.

Talk to a Bank Statement Loan Expert (Fast Review)

Ready to see what you qualify for? Get a quick, no-pressure review of your last 12–24 months of deposits and we’ll match you with the right bank statement loan program.

A bank statement loan is usually a Non-QM (Non-Qualified Mortgage) option.

Bank statement loans are non-QM loans. Instead of income tax returns, mortgage underwriters use alternative methods to calculate your qualified income. Mortgage underwriters average 12 months of deposits of your personal or business bank statement deposits on bank statement loans. Many business owners and self-employed borrowers can qualify by showing 12 or 24 months of business or personal bank statement deposits. Bank statement loans are made for people with real income that is hard to prove in the usual way, such as:

- Self-employed people (1099, sole proprietor, LLC, S-Corp)

- People who earn a living on commission

- Business owners with significant write-offs

- Individuals with variable monthly income

- People who have been paid via deposits (not through payroll)

The Working Mechanism of Bank Statement Loans

Step 1. You Decide Which Statement You Would Use

- Personal bank statements work well if your deposits come in regularly and predictably.

- Business bank statements are a good choice for business owners who want to show their company’s income.

- Sometimes, lenders will accept both personal and business statements, depending on their rules.

- The lender figures out your qualifying income.

- Rather than tax returns, underwriters average your income deposits to estimate your monthly earnings.

Here’s how Bank Statement Mortgage Loans Work:

- For personal statements, lenders add up your eligible deposits, average them, and make small tweaks if necessary.

- For business statements, lenders average your deposits and then subtract a percentage for expenses, usually between 50% and 80%, based on your paperwork and their rules.

- Lenders only use deposits on bank statements and not withdrawals.

Lenders usually do not count these types of deposits:

- Transfers between accounts.

- Loan proceeds.

- One-time unusual deposits without explanation.

- Cash deposits that cannot be sourced or justified (depending on the program)

Step 3: The lender checks for a steady, reliable income pattern. Writers will consider:

- Consistent deposits over time.

- Business activity consistent with your profession.

- Documentation confirming self-employment.

- Large deposits that are supported by contracts or invoices, if required.

Step 4: You’ll also need to meet rules for debt-to-income ratio and other important factors.

On the bank statement review, lenders will check if you qualify based on:

- Credit profile.

- Down payment amount.

- Reserves (money left after closing).

- Type of property.

- Debt-to-income ratio, which can be different for each lender

What Are Bank Statement Loans?

Who Are Bank Statement Loans Best For?

Bank Statement Loans benefit self-employed borrowers with their own businesses who take advantage of IRS tax loopholes and often utilize tax loopholes of business owners. Self-Employed Borrowers With Large Write-Offs and lower adjusted gross income are ideal candidates for bank statement loans.

- If your business tax returns look low because of legal write-offs, a bank statement loan could be a better choice, as it shows your real cash flow.

- If you get paid directly by clients, underwriters may be more flexible with bank statement loans than with traditional, tax return-based options.

Owners of Businesses with Less Clear Finances

- If business profits are hard to show on tax forms because your finances are complicated, a bank statement loan might give you a better chance.

Here’s what most programs expect from borrowers: Most programs ask for:

- 2 years of self-employment history, or

- 1 year with strong supporting documents and prior experience in the same field

Bank Statements

- 12 months of bank statements (this often means a higher down payment or rate)

- Or 24 months (this usually gets you better terms)

Minimum Credit Score On Bank Statement Loans

- Minimum credit score requirements vary by lender and depend on risk factors.

- At Mortgage Lenders For Bad Credit, our minimum credit scores on bank statement loans is generally 580 credit score.

- Remember that the higher your credit score, the lower your rate.

- The lower your loan-to-value, the lower your rate.

- Rates on bank statement loans are based on layered risks lenders take.

Lower Credit Score Borrowers:

- Applicants with lower credit scores may still qualify if they demonstrate compensating factors, such as a larger down payment, substantial reserves, or strong bank statements.

Initial Payment

- Amount of the loan

- Type of statements (personal vs. business)

- Type of risk, such as new credit problems or high debt-to-income ratios

Cash Reserves

- 3 to 12 months of housing payments in savings after closing, depending on the program

Documentation You May Be Required To Provide

- Letters explaining large deposits, if needed

- Standard mortgage documents, such as your credit report, appraisal, title, and insurance

Bank Statement Loans Eligibility Requirements

Important Eligibility Criteria

- Self-Employment: At least 2 years in the business.

- Bank Statements: 1–2 years of regular (monthly) deposits.

- Credit Rating: Some lenders accept credit scores as low as 500, though applicants with scores above 620 usually receive better terms.

- Down Payment: Down payments typically range from 10 to 20 percent, depending on credit score and loan program.

- Debt-to-Income (DTI) Ratio: Most lenders allow a DTI ratio up to 50 percent, with some exceptions.

- This shows you have enough funds to cover 6 to 12 months of mortgage payments. tion

- Personal and business bank statements.

- Profit and loss statement (if it exists).

- Business ID and proof of self-employment (business license).

- Reserves statement.

Which Property Types Can You Purchase Using Bank Statement Loans?

- Primary residences

- Secondary residences (depends on program)

- Investment properties (depending on the program). You can usually purchase the following property types:

- Single-family homes

- Condominiums, though some may need a project review

- 2- to 4-unit properties, though these often have extra rules

Ideal Borrower For Bank Statement Loans

- No Income Tax Documentation Required: This option suits self-employed individuals with substantial income.

- Loan Options for Applicants with Bad Credit: Poor credit history does not automatically disqualify you.

- Potentially Larger Loans: Some programs provide jumbo loans for higher amounts.

- Expedited Approval Process: Approval timelines are often shorter than with traditional loans.

Rates and Costs on Bank Statement Loans

Because bank statement loans are Non-QM, expect higher interest rates than regular loans. The extra risk and special approval requirements make bank statement loans more expensive.

- You might also see higher lender fees, especially if your finances are complicated or the lender has stricter rules.

- However, many people like this option because it makes buying a home possible when regular paperwork is not enough, even for those with a lot of income.

- If you qualify, regular or government-backed loans usually have better rates.

- But when paperwork is a problem, bank statement loans are a good backup.

- You might even switch to a different loan later if your situation gets better.

More About Bank Statement Loans

- Many programs have no tax return stipulations.

- Self-employed borrowers and those with 1099 income can benefit.

- Helpful when write-offs lower your taxable income.

- They are especially helpful if write-offs make your taxable income smaller.

- Also, the paperwork requirements are less strict than for regular loans, but stricter than for QM loans.

- Usually, down payment and savings rules are higher.

- Make sure your deposit records are clear and consistent.

- Remember that not every lender offers a full bank statement review, and most have extra rules.

Bank Statement Loans Compared with Standard Loans

- Bank Statement Income is based on your deposits over 12 to 24 months, which is a big help for self-employed people or anyone with income that changes.

- You will have less paperwork and fewer rules.

- Non-QM pricing and regulations

Conventional, FHA, VA, and USDA Loans

- Income is calculated based on tax returns, W-2 forms, and pay stubs.

- You’ll often get lower interest rates.

- Approval rules are the same for everyone.

- These loans work best for borrowers who can easily prove their income with standard documents.

How Do Bank Statement Loans Function?

The process typically includes these steps:

- Bank Statements Submission: You need to provide at least 12 months of personal or business bank statements.

- Income Calculation: Lenders review your deposits to determine your average income.

- Credit Evaluation: Some lenders consider factors beyond your credit score and are often more flexible than traditional mortgage providers.

- Down Payment: A larger down payment, typically 10 to 20 percent, is required compared to standard mortgages.

- Approval & Closing: Once your information is verified, you may receive financing for a purchase or refinance.

How to Improve Your Odds of Getting Approved for Bank Statement Loans

Keep your deposits organized and easy to track.

- Try not to mix business and personal deposits if you can.

- If you have an unusual deposit, show proof with an invoice or contract.

- Unless your lender says otherwise and you can prove its source, keep cash deposits to a minimum.

Improve Your Credit

- Even a small increase in your credit score can help you get approved and get a better rate.

- Make sure you have enough savings, too.

- Lenders will also look at your finances after closing.

- The less risky you seem, the better your chances of getting approved.

Maintain a Consistent Banking Practice

Frequently Asked Questions About Bank Statement Loans

Are there bank statement loans for people with bad credit?

- Yes. Some lenders work with applicants who have bad credit.

- Mortgage Lenders For Bad Credit are experts on bank statement loans with bad credit.

What is the minimum income requirement?

- Income is based on average bank deposits.

- You must have enough cash flow to cover mortgage payments and existing debts.

How Are Interest Rates On Bank Statement Loans

- Interest rates are usually higher than conventional loans, but remain competitive compared to other non-QM options.

How long does approval take?

- Once all required documentation is submitted, approval typically occurs within two to four weeks.

Is There a Minimum Credit Score for Bank Statement Loans?

- Lenders use different criteria and assess the overall borrower profile, including down payment, credit score, credit history, debt-to-income ratio, and property type.

- Compensating strengths may allow qualification despite a lower credit score.

Bank Statement Loans: Do I Have to File Taxes?

- Many bank statement loan programs allow qualification without tax returns.

- However, in some cases, such as business verification or specific underwriting requirements, lenders may request tax documents even if they are not used for income qualification.

Most programs require 12 or 24 months of bank statements.

- Providing 24 months of credit history may strengthen your application by demonstrating consistent financial behavior over a longer period.

Can I Use Business Bank Statements in lieu of Personal Bank Statements?

- Yes.

- Many lenders allow self-employed borrowers to use business bank statements, but they may adjust gross deposits to account for business expenses.

Are bank statement loans only for self-employed borrowers?

- Most bank statement loans are designed for self-employed, 1099, or commission-based borrowers who do not have traditional income documents.

Can I buy an investment property with bank statement loans?

- Some lenders allow investment properties, but the requirements are usually stricter, with higher down payments, more cash reserves, and tighter credit standards.

- Large or inconsistent deposits do not necessarily preclude approval.

- Applicants may need to document the source of such funds, for example, through invoices, contracts, or business revenue records, to ensure underwriter acceptance as qualifying income.

Are bank statement loans harder?

- Some bank statement loans may be more challenging to close due to the need for detailed documentation.

- Underwriting focuses on deposit history, consistency, and clear records rather than tax transcripts.

- Well-organized statements help facilitate a smoother approval process.

Can I refinance out of a bank statement loan later?

- Refinancing into a conventional or government loan is possible if your credit and documentation improve, which may result in lower rates and payments.

- Eligibility also depends on market conditions and your documentation at the time.

Why Do Banks Deny Mortgage Loans?

- Common reasons for loan denial include undocumented large deposits, negative balances or overdrafts, irregular deposit patterns, and excessive debt-to-income ratios.

Bank statement loans can be a strong option for individuals with bad credit if they have:

- Real income

- Real ability to repay

- Valid explanations for why they do not “look good on paper.”

Bank Statement Loans are an Option for self-employed individuals,

those compensated through deposits, or applicants whose tax returns do not meet qualification standards. You can speak with a loan analyst about your deposits over the past 12 to 24 months, your credit, and down payment options to find the program that fits your goals, often a bank statement loan. Review your bank statement loan options with Mortgage Lenders for Bad Credit at 800-900-8569 today. Text us for a faster response.

What is the benefit of working with Mortgage Lenders For Bad Credit?

- Multiple bank statement loan lenders so we can get the best rate and terms on your loan.

- Dedicated support for applicants with bad credit, transparent fees, and clear contract terms.

- Self-employed applicants benefit from higher approval rates.

Get Your Bank Statement Loan Options (Even If You Were Denied)

If your tax returns don’t reflect your real income—or you’ve been turned down elsewhere—let’s look at your cash flow and build a clear path to approval with a non-QM bank statement loan.