Mortgage Financing For Foreign Nationals

Financing A Mortgage For Foreign Nationals

Learn how foreign nationals can qualify for a mortgage, including visa requirements, documentation, down payments, and more with Gustan Cho Associates. Getting a mortgage as a foreign national can be complicated. Although foreign buyers are important to the U.S. housing market, lenders are often cautious due to factors such as visa status, limited or no U.S. credit history, income from foreign sources, and additional paperwork requirements. John Strange, a senior mortgage loan originator at Mortgage Lenders For Bad Credit says the following about mortgage financing for foreign nationals:

Comprehensive Mortgage Financing For Foreign Nationals In The U.S., including eligibility requirements, loan programs, and how to get a mortgage without a U.S. credit history.

The team at Mortgage Lenders For Bad Credit helps foreign nationals achieve home ownership. Mortgage Lenders for Bad Credit, a wholly-owned subsidiary of Gustan Cho Associates, helps foreign nationals find the right mortgage options. Many lenders do not offer these programs, so this guide offers a clear overview of the process, main requirements, and steps for a successful application. Let’s explore key elements of foreign national mortgage financing.

Mortgage Financing for Foreign Nationals includes

Mortgage financing for foreign nationals refers to loans issued to non-U.S. citizens who are eligible if they are:

- Visa holders (i.e., students, workers, etc.).

- Non-residents of the U.S. who purchase U.S. real estate while staying outside the U.S.

- Recently arrived in the U.S. and have very little U.S. credit history.

Foreign National and Want to Buy in the U.S.? We Can Help

No green card? No Social Security number? You may still qualify. Call Gustan Cho Associates at 800-900-8569 and ask about our foreign national mortgage financing programs for primary, second homes, and investment properties

Financing Problems Facing Foreign Nationals

Foreign nationals seeking mortgage financing in the U.S face problems that domestic borrowers rarely face. The biggest challenge is the lack of U.S credit history. Most traditional lenders and investors rely on credit history to determine risk. This mostly applies to FICO scores and reports. Because of this, foreign nationals often face rejection on a blanket basis in U.S. traditional mortgage programs.

Additionally, foreign nationals often lack U.S. employment history and tax returns, which makes the process even more challenging to qualify for a mortgage. Most lenders face foreign borrowers as a higher risk, and for a good reason.

Consider the following: Can you mitigate any of these risks and still maintain a good situation at home? Currency risk in your home country, such as political instability, or the need to relocate to your home country. For these reasons, foreign nationals face unprecedented challenges in traditional mortgage financing.

Underwriting Guidelines Facing Foreign Nationals

Foreign national borrowers are subject to different underwriting rules. Lenders typically review the following:

- Visa or residency documentation and its legal status.

- Income sources within the U.S. or outside the U.S.

- Credit report.

- Documentation of assets, their movement and transfer, and their sources.

Considerations for Different Types of Foreign Nationals Getting a mortgage

Depends on where you live, your visa or residency status, and your plans for the property. Knowing these details helps you find the best loan options.

Foreign National Loans for Non-Residents Living Outside the United States

This program is designed for buyers who:

- Are based outside the U.S.

- Are interested in purchasing a house or condominium in the United States.

- May not have a Social Security Number

Common features:

- Increased down payment

- Different credit documents

- Proof of wealth and savings

- Careful checks of your identity and money sources

Programs For Foreign Nationals With A Visa

Some visa holders may qualify the same way as a U.S. resident, depending on:

- Visa type and duration

- Work history and income consistency

- U.S credit and Even if some applications are declined, some lenders will work with visa holders who provide complete and accurate documents and documentation.

U.S. real estate can also be:

- If you plan to purchase a rental property, a larger down payment is typically required.

- Significant reserves

- Documented income and asset sources

Now, let’s summarize the key qualification points common to most foreign national mortgage programs. While each one has distinct requirements, most lenders emphasize similar primary criteria.

Minimum down payments required depend on:

- Residency status: (Resident vs. non-resident).

- Credit profile and strength of documentation.

- Type of property (single-family homes, condos, multi-units).

- Type of occupancy (primary, second Most foreign national mortgages need a larger down payment than regular loans.

- Lenders may look at your U.S. credit history or other ways to show you pay bills on time.

- International credit references (where accepted).

- Other ways to show credit, like paying utility bills (gas, electric, water).

- Mobile phone payment.

- Rental payment verification.

- Applicants lacking sufficient U.S. credit history may still qualify by demonstrating on-time payments using alternative documents.

- Proving income is also important for foreign nationals employed in the United States.

- A letter from your employer verifying your employment.

- Income documents from overseas (translated if necessary).

- Tax returns (American and for foreign countries).

- Bank statements that show a certain program’s permit qualification based on assets or bank statements rather than tax returns.

- This approach is particularly beneficial for self-employed borrowers residing outside the United States. Rules

The lender must verify the following:

- The source of your down payment funds.

- The funds are legitimate and document.

- Wire transfers must follow U.S. banking and anti-money laundering rules.

- These rules need a clear paper trail. Giving complete documents can make your mortgage approval process smoother.

The type of visa you hold will influence:

- The different programs you may qualify for.

- The requirements for down payments and reserve requirements.

- The documentation required.

- The need for an SSN or ITIN.

Moving on, let’s address a common question: Can you get a mortgage without an SSN?

- Yes, many loan programs allow qualification without an SSN, if you use an ITIN or other accepted ID.

- Eligibility depends on program terms and property type for non-resident foreign nationals investing in U.S. real estate.

- Review each program’s requirements before applying.

- Stand-alone single-family homes.

- Approved condos.

- Townhomes.

- 2–4 unit residential properties (on a case-by-case basis).

- Certain vacation homes or second homes.

- Investment properties.

Denied Because You’re Not a U.S. Citizen or Permanent Resident?

Many banks don’t know how to work with foreign nationals—we do. Contact Gustan Cho Associates and let us review your passport, visa, and assets for specialized foreign national mortgage financing

Some properties are more challenging to finance for foreign nationals, such as:

- Unique homes with customized features that make market value difficult to determine

- Condos with a high percentage of units owned by real estate investors

- Rural properties that have few or no recent sales.

Challenge 1: Limited U.S. Credit

- Solution: Provide alternative credit documentation, establish U.S. tradelines, and demonstrate strong financial reserves.

- Navigating documentation and banking requirements can be complicated.

- Here are practical solutions: submit translated documents, provide clear employment verification, and maintain consistent banking records.

- Plan ahead and ensure a clear paper trail for all financial transactions.

- Partnering with a lender experienced in foreign national loan programs can help navigate requirements and assemble the necessary documentation for your application.

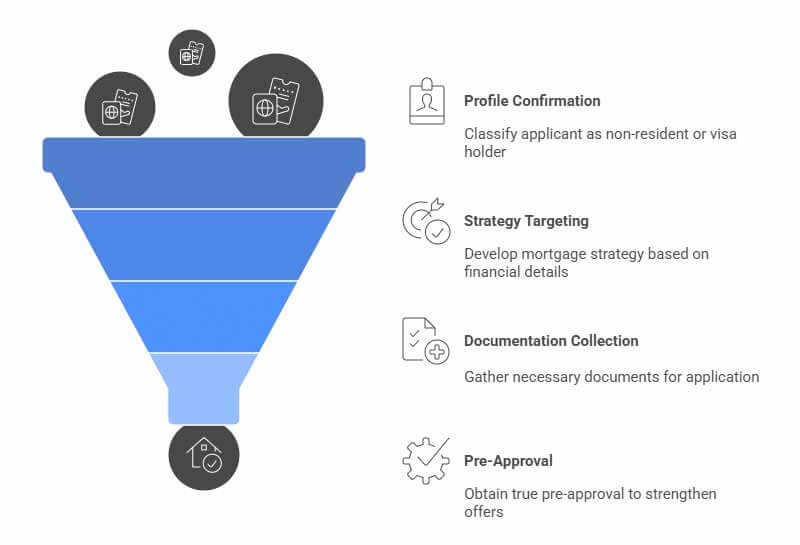

- Next, let’s outline key steps in the application process.

Step 1: Confirm Your Buyer Profile

We will classify you as:

- Non-resident foreign national

- Visa holder / non-permanent resident

- Investor or owner-occupant

Step 2: Target Best Mortgage Strategy

We will build a profile of your program based on:

- Down payment

- Credit options

- Income type (salary, self-employed, overseas)

- Target properties

After selecting a mortgage strategy, continue to Step 3: Collect Initial Documentation and visa (if applicable).

- Proof of residency abroad or U.S. address (depends on program)

- Bank statements (domestic and/or international)

- Proof of income (employment letter, pay stubs, business income), investments, and reserves

Step 4: True Pre-Approval Instead of Pre-Qualification

A true pre-approval enables applicants to make stronger offers and demonstrates financial readiness to sellers.

- Choose a lender experienced in foreign national loans to avoid unforeseen conditions later. Closing may involve additional steps, such as verifying international wire transfers.

- Identity verification and compliance.

Mortgage Lenders for Bad Credit: Foreign National Mortgages

Many mortgage lenders can assist foreign nationals, but some avoid these loans due to the additional documentation and a more complex review process. In unusual situations, including:

- Borrowers with no U.S. credit history, self-employed foreign nationals

- Review of foreign income Approvals with alternative documents

- Strategies for financing investment properties.

- As part of the Gustan Cho Associates network, we focus on finding solutions, especially when other lenders are unable or unwilling to assist.

- Income is earned abroad.

- You are purchasing property from abroad.

- You have received a “no” answer from a bank.

Mortgage financing for foreign nationals is doable, even when:

- Long U.S. credit history is non-existent.

- Income is earned abroad.

- You are purchasing property from abroad.

- You have received a “no” answer from a bank.

The most vital components consist of:

- Clean Documentation

- Assets/income that are verified

- A realistic down payment plan

- A lender that specializes in foreign national programs

- Foreign national applicants benefit from working with lenders who specialize in mortgage programs tailored to their needs.

Use Global Assets to Qualify for a U.S. Home Loan

Income and assets from outside the U.S. can often be used with the right program. Call 800-900-8569 and learn how our foreign national mortgage options can leverage your international income and banking

To conclude, here are answers to frequently asked questions:

Can a foreign national get a mortgage in the U.S.?

- Yes, foreign nationals can obtain a mortgage in the U.S.

Do I need a Social Security Number to get a mortgage?

- Not always.

- Most foreign nationals do not require an SSN.

- Some programs require an ITIN, or other acceptable ID, and some foreign national programs do not require an SSN.

What down payment is required for mortgage financing for foreign nationals?

- It depends on residency, credit history, and property type.

- Compared to conventional loans, foreign national loans usually require a larger down payment.

- The income must be verifiable, documented, and meet program guidelines.

- Documented translations are useful.

Can foreign nationals buy investment property with a mortgage?

- Yes.

- Many foreign nationals obtain financing for rental properties or vacation homes.

- However, these loans often come with more restrictions than those for a primary residence.

- Typical documents include a passport, visa (if applicable), bank statements, proof of assets, and income verification for both the U.S. and your country of residence.

Can I get approved if I don’t have U.S. credit?

- It is possible.

- Some lenders consider comparable credit histories or other forms of payment history.

What is my visa type?

- Your visa type and length of stay may determine which mortgage options are available and the required documentation.

Can I close on a home if I live outside the U.S.?

- Generally, yes. Many international buyer programs are designed for clients living outside the U.S. Closing logistics include notarizations and international wire verifications.

How long does the foreign national mortgage process take?

- Timelines vary, but foreign national mortgage processes typically take longer than standard mortgages due to additional documentation, sourcing funds from abroad, and compliance requirements.

Can I use money given to me as a gift from family overseas for the down payment?

- Sometimes, depending on the mortgage program. Gift funds must be documented and have a clear paper trail for the transfer to be processed.

What’s the best first step to get mortgage financing as a foreign national?

- The best first step is to review your residency status, income type, assets, and property goals to match you with the most suitable program.

Get Approved for Mortgage Financing For Foreign Nationals

If you are prepared to purchase a home or investment property in the United States, our team can help you identify the most effective path to approval, even if previous attempts have been unsuccessful.

Contact Mortgage Lenders for Bad Credit (a Gustan Cho Associates company) today to discuss mortgage financing for foreign nationals, down payment options, and qualification requirements.

Start Your Foreign National Mortgage Pre-Approval Today

Whether you’re buying a vacation home, student housing, or a rental, we have options. Apply online 24/7 with Gustan Cho Associates and see how close you are to mortgage financing as a foreign national buyer in the U.S.