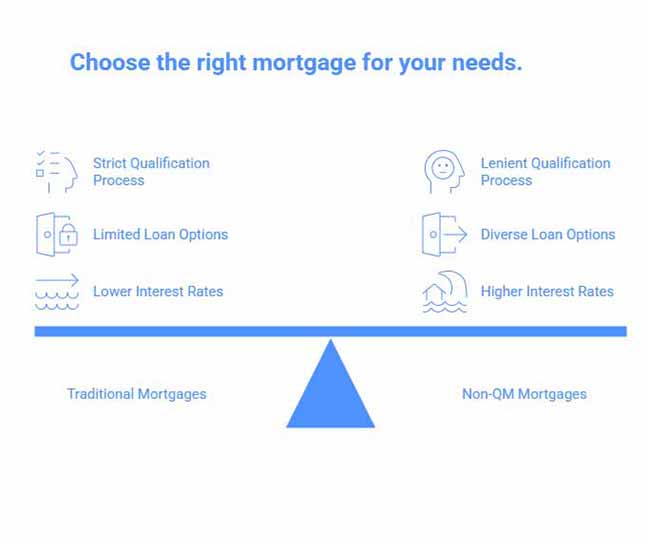

Non-QM Versus Traditional Mortgages

Non-QM Versus Traditional Mortgages: Understanding the Key Differences

Are you considering acquiring a mortgage but don’t know where to start? Perhaps you have an unconventional income source that has left you questioning whether you qualify for financing. Or perhaps you have had some difficulties with mortgages that you don’t wish to repeat. If so, you’re probably searching for some information on the different varieties of mortgages, such as non-qualified mortgages and traditional mortgages. This article will outline what you should consider for both so that you can choose what works for you.

What are Traditional Mortgages?

A traditional mortgage loan is known as a Qualified Mortgage (QM) and must adhere to strict criteria established by government-backed entities such as Fannie Mae and Freddie Mac. This ensures that one can afford the mortgage loan, which reduces associated risks.

Important Attributes of Conventional Mortgages:

- Formal Documentation Requirements: W-2s, tax returns, pay stubs, employment verification

- Hard Debt-to-Income (DTI) Limits: Generally set no higher than 43%

- Credit Score Requirements: Typically 620+ with Higher Credit Scores Required for Best Rates

- Income Verification: The importance of stable, predictable, and verifiable income

- Standardized Underwriting: Adheres to agency guidelines with little flexibility

Not Sure If You Need Non-QM or a Traditional Mortgage?

Call Gustan Cho Associates at 800-900-8569 and let us compare non-QM versus traditional mortgages side by side for your real numbers.

What are Non-QM Mortgage?

In the Non-QM loans can be termed as loans that are not based on the conventional terms offered by the common lender. They provide people who may have different financial circumstances a chance to purchase a house when they may not meet the conventional terms.

Main Features of Non-QM Loans:

- Flexible Documentation Options: Bank statements, 1099 forms, asset statements, Profit and Loss statements

- Accommodating DTI Ratios: Usually has higher debt-to-income ratios

- Credit Flexibility: Although it is still valuable, its criteria become less strict for consumers experiencing current credit activities

- Alternative Income Verification: Open to nontraditional income sources and verification.

- Customized Underwriting: Involves an approach to loan applications that looks at the financial condition of the borrower from a wider

Documentation Requirements

- Traditional: It requires several years’ worth of W-2 statements, tax returns, and employment history

- Non-QM: Accepts alternative methods of documentation such as bank statements, Asset qualification, or DSCR for investment properties

Who Benefits from Each Mortgage Type?

Conventional Loans Work Best For :

- W-2 employees with stable, verifiable income

- People with good credit ratings and a low debt service/ income ratio

- Purchasers who buy their first home and qualify for standard home buying qualification criteria

- Those in pursuit of possibly low-interest rates and standardized terms

Non-QM Mortgages Are Suitable For:

- Entrepreneurs and self-employed professionals

- Freelancers, gig economy workers, and variable income earners

- Real Estate Investors (specifically through DSCR Loans)

- Borrowers with recent credit events, but good finances overall

- Foreign Nationals Investing in the U.S. Real Estate Market

- Individuals with considerable assets but inadequate documented income

Speed and Efficiency Comparison

Traditional Mortgages: Typically longer because of extensive background verifications

*Non-QM Loans: Potentially close quicker (as quickly as in 2-3 weeks) because of simplified documentation and the lack of agency involvement

Rates of interest and costs

* Traditional Mortgages: Typically involve lower interest rates as the risk is perceived as lower.

* Non-QM Mortgages: Slightly higher rates required to mitigate added flexibility and risks associated with Non-QM mortgages.

* Market Evolution: “The spread between Non-QM loans and conventional loans has decreased substantially over time, due largely to the maturation of the Non-QM market”

See the Payment Difference: Non-QM vs. Traditional Loan

Contact Gustan Cho Associates for a custom comparison of non-QM versus traditional mortgage options so you can decide with real data

Non-QM Versus Traditional Mortgages

NQM resembles conventional mortgages As already mentioned, there are tough requirements you must qualify for in order to secure the traditional mortgage. The lender will want to review your income and debt payments to determine if you are eligible. This means that you must submit quite a bit of paperwork to qualify you as being creditworthy. The waiting process can be quite long. If you are looking to qualify quickly, then the traditional mortgage may not be your best choice. It is usually quicker to qualify with the non-QM loan. In most cases, the traditional lender can refuse to deal with respectable investors in the event that they don’t have the required documents or meet all the necessary qualifications. That being said, with a Non-QM lender, the lender is more lenient in the process and can consider clients who possess a sound credit rating, assets, or even experience in investments. This provides you with an enhanced possibility of acquiring a home loan compared to the traditional lender. Non-QM mortgages provide various options like asset backed loans, bank statement loans, investor cash flow loans, jumbo loans, 1099 income loans, foreign national loans, and ITIN mortgages. This enables you to choose the one that will suit you in the best way according to your needs. The rate of interest as well as the fees involved in taking Non-QM loans will be a little high compared to other types of loans since Non-QM loans are not insured by the government. A good broker will assist you in getting the best option.

Conclusion

Non-qualified mortgages are another alternative to traditional mortgages. This form of mortgage will work well in situations where the applicant is self-employed or has difficulty substantiating income. In addition, non-qualified mortgages will benefit applicants that have issues with their current credit score. Nevertheless, non-qualified mortgages have higher interest rates compared to other types of mortgages, which means one must evaluate their choices accordingly. Nevertheless, if one chooses to apply for non-qualified mortgages, a professional mortgage broker will be essential in procuring the best deal.

FAQs: Non-QM Versus Traditional Mortgages

- Q.1 In what ways do traditional mortgage loans compare to Non-QM mortgage loans?

Traditional mortgage loans are based on specific criteria, including income, employment, credit score, and debt-to-income ratio. The Non-QM mortgage loan offers flexibility in documentary verification of income, allows for an increased debt-to-equity ratio, and considers lower credit scores and unconventional income sources. - Q.2 Who can benefit from a Non-QM loan?

Non-QM loans are most suitable for self-employed borrowers, real estate investors, borrowers with non-traditional sources of income, or individuals seeking a loan who cannot qualify for a traditional loan. - Q.3 Are interest rates higher in Non-QM loans?

Yes, typically, interest rates in Non-QM loans are higher compared to traditional loans. Higher interest rates on Non-QM loans help offset the risks involved with such flexible loans. - Q.4 What are the requirements for a Non-QM mortgage?

Since a Non-QM mortgage doesn’t require the submission of pay stubs, W-2 forms, and tax returns, like regular mortgage requirements do, to verify income and stability, alternative sources such as bank statements or proof of assets may be used. - Q.5 Is it possible for me to obtain a Non-QM loan with bad credit scores?

Non-QM lenders tend to be more flexible in their credit standards. This means that borrowers with a history of bankruptcy, foreclosure, and/or poor credit can also be eligible. - Q.6 How do I choose the right mortgage for me?

Think about your steady income, credit ratings, and your capacity for standard financial documentation. Take advice from a mortgage expert. - Q.7Are Non-QM loans safe?

Non-QM loans can be safe if sourced from reputable lenders and are in compliance with federal and state laws. This is because, like any type of loan, one must understand what is involved in a Non-QM loan and seek advice from a reputable mortgage consultant.

Get a Personalized Strategy, Not a One-Size-Fits-All Answer

Apply online 24/7 with Gustan Cho Associates and get a side-by-side breakdown of non-QM versus traditional mortgages tailored to your credit, income, and long-term plans

This blog about “Non-QM Versus Traditional Mortgages” was updated on December 22th, 2025.