One Time Close Construction Loans: One Loan, One Closing, From Building to Moving In

Building a home and getting financing can seem overwhelming. A One-Time Close Construction Loan, also known as a single-close or construction-to-permanent loan, simplifies the process by combining construction and mortgage financing into a single loan with a single closing. GCA Mortgage Group, a wholly-owned subsidiary of Gustan Cho Associates, can sometimes cause confusion for borrowers and builders with its detailed information about loan draws, underwriting, appraisals, and timelines. This guide on one time close construction loans explains how One Time Close Construction Loans work, the timeframe involved, who qualifies, and what lenders expect. You’ll find a simple, step-by-step explanation of the process from approval to closing.

What Are One Time Close Construction Loans

A one-time close construction loan is a mortgage that finances:

- The land purchase (if needed)

- Construction costs

- The mortgage is paid when the home is done.

With a One-Time Close Construction Loan, you don’t need to get a short-term construction loan and then refinance later. You close once, and when construction is complete, the loan automatically converts to a regular mortgage.

Build From the Ground Up With Just One Closing

Call Mortgage Lenders For Bad Credit at 800-900-8569 to see if you qualify for a one time close construction loan

Type of One Time Close Construction Loans

A One-Time Close Construction Loan is a type of coverage (with a single closing) that can be done under different mortgage lines. The major differentiation among these options lies in occupancy regulations, down payment expectations, credit and income flexibility, property types, and builder requirements.

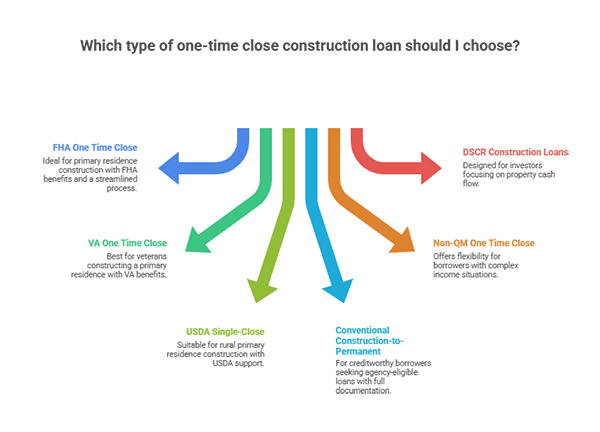

FHA One Time Close Construction-to-Permanent Loans

Streamline FHA One Time Close Construction-to-Permanent loans by integrating the lot (if needed) and closing on the combined construction and permanent FHA mortgage on one occasion. These loans often apply to primary houses under construction, appealing to borrowers who want FHA benefits with the simplicity of a single close. One-time closes, as the name suggests, are handled differently from two-step closes. Best for: Buyers seeking an FHA-backed, primary residence, build-to-move-in loan who want a streamlined, one-time closing process.

VA One Time Close Construction Loans

VA one time close construction loans enable qualified veterans to finance both construction and permanent loans in a single closing, transitioning directly to a long-term VA mortgage after completion of the construction phase. VA loans have unique guidelines for one-time and two-time construction loans, which apply to primary residences and are subject to VA underwriting and guaranty. Best for: Eligible veterans seeking to construct a primary residence while utilizing VA benefits in a single closing process.

USDA Single-Close Construction-to-Permanent Loans

USDA Rural Development offers USDA One Time Close Construction-to-Permanent option within its single-family housing programs and through its partner lenders. The USDA provides a dedicated fact sheet on this type of financing, which has led to the term “USDA one-time close construction loan” being used in the market. Best for Market: All individuals who would like single close construction-to-permanent financing in the USDA loan program.

Rural Development

Best for: Buyers eligible for USDA loans who seek a primary residence in a rural area and prefer the simplicity of a single-close build.

Conventional Construction-to-Permanent Loans

Conventional (non-government) one-time close loans are commonly referred to as single-close construction loans. On the agency side, Fannie Mae’s Selling Guide covers single closing construction-to-permanent transactions, where the construction phase leads directly to permanent financing in a single closing.

Best for: Creditworthy borrowers seeking agency-eligible one-time close construction loans with full documentation.

Non-QM One Time Close Construction Loans

Non-QM construction loans are portfolio/non-agency options that can be structured as one-time closings through certain lender programs. In this structure, once the construction phase ends, the loan converts directly to permanent Non-QM financing, requiring only one closing. They are useful when the borrower requires flexible income documentation, such as for self-employed individuals or those with variable or complex income streams. Because Non-QM loans are lender or investor-specific, their requirements are broader and more varied than those of FHA, VA, USDA, or Conventional loans.

DSCR Construction Loans

At some level, DSCR is an investor method (qualifying mostly on property cash flow rather than personal income. DSCR construction loans are typically Non-QM or portfolio products, not conventional agency loans. In the one-time close format, the loan finances construction and, after completion, automatically transitions to a permanent DSCR loan—though availability is limited, and guidelines can vary widely. Construction-to-perm is allowed.

Important clarification: FHA 203(k) typically is not “one-time close construction.”

FHA 203k Loans

FHA 203(k) loans is often part of construction loan discussions, but it is usually a rehab or renovation mortgage. It is for buying, repairing, or refinancing an existing property. It is not a ground-up new construction one-time close like FHA Construction-to-Perm. The FHA 203(k) remains relevant because it helps people searching for both building and renovation solutions, and keeps them interested in your site.

One Time Close vs. Two Time Close Construction Loans

On Two Time Close Construction Loans, You Get To:

- Close on a construction loan

- Pay your closing costs on the construction.

- Consider a permanent mortgage later, and you may likely get a worse deal.

On One Time Close Construction Loans, You Get To:

- Close once on your construction and mortgage

- Lock in your terms with the lender.

- After the loan is done, you don’t need to close again for permanent financing.

Turn Your Lot and Plans Into a Finished Home With One Loan

Reach out today and let us structure a one time close construction-to-perm mortgage for your project.

How One Time Close Construction Loans Work

A One-Time Close Construction Loan requires you to have an approved builder, a set construction plan, an estimated budget, and a draw system. The draw system allows funds to be released in stages as the home is being built.

A Step-By-Step Overview

- You choose your builder and lot: This could be a lot you already own, land you are buying, or sometimes a teardown and rebuild, depending on the program rules.

- Construction plan, specifications, and budget: Your lender will need a detailed breakdown that includes the construction plan, a list of materials, and the full estimated budget.

- This is often referred to as a line-item cost breakdown or a builder’s bid.

- You close once: When you close, the loan covers both the construction and the permanent mortgage.

Construction Begins, and Funds Are Released Through Draws

Money is given out in stages, called draws, as the work is completed and inspected.

- The home is complete, and the loan switch is now finalized.

- After the final inspection and receipt of the Certificate of Occupancy, the loan converts to a permanent mortgage.

How Payments Work During The Construction Period

With these loans, you usually pay interest only on the money that has been used during construction, not the whole loan amount.

Once construction is complete, the loan converts into a regular mortgage, with payments that include principal, interest, taxes, and insurance.

Variations of One Time Close Construction Loans

Flexible Options Allow For Various Structures on One Time Close Construction Loans. Common Variation Types Include:

- Regular construction to permanent loans: These loans are typically best suited for individuals with good credit, a steady income, and standard occupancy needs.

- Government-supported options (varies by program): Some borrowers can qualify using government guidelines, depending on the lender and the loan program.

- Non-QM construction options (if available): For self-employed borrowers or those with atypical income situations,

it may be possible to have an easier documentation process, which will depend on the lender and the product. Because rules and availability for one time close construction loans vary by state and investor, GCA Mortgage Group members often compare loan types, builder requirements, and draw processes to determine the best options. The team at GCA Mortgage Group tires to ensure that you select a program that meets your specific needs.

Mortgage Process for One-Time Close Construction Loans

With these loans, there are the “normal mortgage steps” that loan officers take, plus some builder construction-related verification steps that require some extra work. Here is the general flow.

Pre-Approval Review

You must give:

- Evidence of your income and your job (or alternate documents as needed)

- Assets to confirm the down payment and reserves

- Credit authorization and a preliminary credit review

- Tax/income verification authorization (when needed)

Builder’s Approval And Construction Documents

The lender will usually ask for:

- The builder’s licensing documents, as well as proof of insurance

- Builder’s credentials (background of previous successful builds)

- Contract between you and the builder

- Architectural documents with a budget

- Anticipated schedule (when to start, key progress dates, and when to finish)

Underwriting With Conditions

Underwriting emphasizes:

- Your potential to pay back (DTI, assets, credit)

- The property’s potential (blueprints & documents, its worth, and its costs vs the value)

- Reviewing the builder’s risks

- The title/land ownership and permits (when needed)

Appraisal (Usually “Subject to Completion”)

The appraisal is usually performed upon:

- The architectural blueprint and documents

- Related new construction sales

- The anticipated worth when done

Closing And Construction Draws

Following Closing:

- Funds are released in draws

- Inspections confirm completion of each segment.

- Final inspection/CO initiates conversion to the permanent phase.

Now, Let’s Look at What You Need To Qualify For One Time Close Construction Loans

Qualifying for these loans depends on the program, but there are typically three main factors lenders consider.

Borrower Eligibility Guidelines

The major ones are:

- Acceptable credit: Credit history requirements vary by program.

- Consistent employment: You will need to provide employment documentation, verifiable income, or alternative approved employment documentation.

- Down payment: You will need sufficient savings to cover the closing costs, plus additional funds.

- DTI: You will need a debt-to-income ratio that falls within the specific program guidelines.

Property Eligibility Guidelines

These are typically the ones that are accepted:

- Primary residences are the most common types that are accepted.

- Sometimes, second residences: it will depend on the specific program guidelines for this.

- Investments: There will be more restrictions on this, especially for newly constructed properties, but it will depend on the specific program guidelines.

Builder Eligibility Guidelines

These are the most common builder eligibility requirements for One Time Close Construction Loans:

- Builders must be approved by the lender and comply with all applicable state regulations for construction, including obtaining proper licensing in accordance with state laws and meeting any additional lender conditions.

- Builders must maintain current general liability and workers’ compensation insurance to cover all employees and subcontractors working on the project. Documentation proving coverage is typically required by lenders.

- Builders must demonstrate a successful track record, including completion of similar projects. Lenders may request references or a portfolio of previous builds to verify experience and reliability.

- A signed construction contract with the builder is required, detailing the full scope of work, cost allocation for materials and labor, and responsibilities for managing the budget throughout the build.

Tired of Competing for Resale Homes? Build Instead

Contact Mortgage Lenders For Bad Credit and we’ll walk you through the entire construction loan process from start to finish

One Time Close Construction Loans Eligibility Qualifications

Each loan type will have different guidelines and requirements, but these are generally the most common categories that all lenders will have at least some representation in, covering these overarching areas.

Credit Requirements

Underwriting will look at

- Credit score and overall credit history

- History of paying your mortgage/rent (THIS IS CRUCIAL!)

- (Depending on the program) Recent late payments, collections, and major derogatory events.

Income and Employment Requirements

You might need

- W-2 Income docs (such as pay stubs and W-2s).

- Self-employment paperwork (like tax returns) or other documentation, depending on the program.

- Employment verification.

- Consistent income history.

Down Payment Requirements

The down payment is based on

- The type of loan program.

- Your credit.

- If you already own the land (land equity may be considered).

- Appraised “as completed” value vs. total costs.

Cash Reserves Requirements

Due to the numerous moving parts involved in construction, many construction programs require reserves. Reserves can help cover:

- Interest that accrues during construction.

- Change orders.

- Cost overruns.

- Delays that push the finish date.

Construction and Builder Documentation

The common items that might need to be submitted are:

- Signed construction contract.

- Plans and specifications that include materials.

- Itemized cost breakdown.

- Draw schedule.

- Permits (these can be timely in some areas).

- Construction insurance documents of the builder.

Timeline on One Time Close Construction Loans: From Start to Finish.

Construction loans typically take longer than purchase loans, as there is a greater amount of paperwork to review.

Here are some realistic time frames you can share on GCA Forums to help set expectations.

Pre-Approval Length

Getting pre-approval usually takes 1-3 business days, unless your income situation is more complex.

- Complexity regarding self-employed income documentation

- Need to document assets or large deposits.

- Credit disputes

How Long Does Underwriting One Time Close Construction Loans Take

1-2+ weeks is reasonable to expect for most situations, depending on:

- Builder approval turnaround

- Completeness of plans/specs and cost breakdown

- Appraisal scheduling and complexity

- Condition items (updated docs, explanation letters, etc.)

Appraisal

1-3+ weeks is standard for new construction, subject to appraisals.

- Limited comparable properties

- Complex custom builds

- Busy appraisal markets

How Long To Close

Many borrowers close in 30-60 days, but 45-75 days is more common for construction loans, especially if builder documents are late or details are missing.

Construction Process Timeline

Closing construction timelines differ significantly from mortgage closing timelines. Depending on the type of build:

Using Production Builder

It is often faster with timelines.

Custom Home Builder

It is often slower with timelines.

Other Factors

Permits, inspections, material availability, and weather can all impact the construction schedule. limit to the build period (generally speaking, 6-12 months, but may be longer depending on the product).\

Delays on One Time Close Construction Loans

Borrowers on GCA Forums often mention the same common problems. It’s best to avoid these from the start. Der fails to provide licensing/insurance or a cost breakdown in a timely manner, and things sort of stop or stall with underwriting.

Multiple Change Orders During Construction Phase

Change orders can have a direct impact on the budget versus the appraised value, resulting in rework and delays.

Reserves Unplanned

Even if you have the down payment, you might still need to meet reserve requirements.

Picking a Lot With an Unknown Title or Access Problems

- Easements, zoning, utilities, or road access issues can prevent a deal from going through or ruin a deal.

- Unrealized Construction financing is more complicated than regular mortgages.

- Plan for a longer closing period to reduce stress.to avoid stress.

One-Time Close Construction Loans FAQs

What Are The Benefits of One Time Close Construction Loans?

- The main benefit is that you only have one closing, one set of closing costs, and your loan automatically converts from construction to a permanent loan with no additional closing required.

- Closing needed.

What Type of Payment is Expected During Construction?

- Most of the time, you are expected to pay an interest-only payment on the amount taken out during the construction period.

- Each program has its unique rules regarding this.

- Once the construction is finished, the loan is converted into a higher, permanent mortgage payment.

Are One Time Close Construction Loans Valid For Land and Construction?

- Yes, many programs allow you to finance both land and construction, as long as the total package meets the program’s guidelines.

Is a Licensed Builder Required?

- Most of the time, the answer is yes.

- The lenders have a builder approval requirement, which involves checking for licensing and insurance.

How Do Lenders Release Funds?

- Lenders release funds using a draw schedule.

- After each inspection confirms the builder has finished a stage, the next payment is made for that stage.

What To Avoid Construction Budget Overruns

- Construction Cost overruns, planning to set aside a budget is the first step in working with the program to reduce reworking the scope and plan.

- Most of the time, you will be expected to bring in the additional funds.

What Credit Score Do I Need for One Time Close Construction Loans?

It varies based on the lender and loan type.

Conventional lenders tend to require higher credit scores than alternative lenders.

Can I Use One Time Close Construction Loans on Investment Properties?

- In some cases, yes, but it’s heavily dependent on the lender and the programs they have.

- Most cases involve the construction of primary residences.

Is The Appraisal Done Before The Home is Built?

- Yes, the appraisal is typically conducted as a “subject to completion” appraisal, which estimates the value based on the home’s plans and specifications.

- The value is checked again when the home is finished.

How Long Does the Entire Process Take?

- It typically takes 30-60 days to close the loan, plus additional time for construction, which can span several months.

Join the Conversation on GCA Forums

- The fastest way to avoid the surprises that come with One-Time Close Construction Loans is to learn from real borrower experiences.

- This can be difficult with the daily situations being documented on GCA Forums.

- For these Construction Loans, they are powered by Gustan Cho Associates.

If you want, I can also create:

A meta description that is 140-155 characters

10 internal-link anchor text ideas for gcaforums.com

A keyword cluster list tailored to your SEO strategy, including primary, secondary, and long-tail keywords.

Get Pre-Approved for a One Time Close Before You Meet Builders

Apply online 24/7 with Mortgage Lenders For Bad Credit and get a solid pre-approval for a one time close construction loan tailored to your plans